How do retail businesses balance payment security and operational efficiency?

Retailers have to protect card data, control fraud, and meet payment obligations without creating slow checkouts, failed terminals, or extra staff work. The right balance comes from tighter scope, cleaner processes, and controls that support speed instead of fighting it.

During a Saturday promotion, Ashton W. watched tokenized card transactions fail after a payment gateway certificate expired on the store controller; three lanes fell back to manual entry, lines stalled, and the combined lost sales, labor, and emergency remediation reached $75,750.

The following scenario is based on a redacted real-world business IT incident pattern. Identifying details have been changed for privacy, but the disruption sequence and cost impact remain realistic.

About the Author: Scott Morris

Scott Morris is an experienced IT and cybersecurity professional with 16 years of hands-on experience in managed technology services. He specializes in How do retail businesses balance payment security and operational efficiency? and has spent his career building practical recovery, security, and operational continuity processes for businesses across Nevada.

This article is intended to help business leaders understand operational tradeoffs in retail payment environments. This is general technical information; specific network environments and compliance obligations change strategy.

- Speed at the lane: Customers abandon purchases when terminals time out, approvals lag, or staff have to fall back to manual entry.

- Security in the background: Tokenization, encryption, least-privilege access, and disciplined updates reduce the chance that a store system becomes the easiest route into payment data.

- Control over exceptions: Returns, offline processing, gift cards, and seasonal staffing are where weak processes usually bypass otherwise reasonable controls.

In practice, retail environments become fragile when stores bolt new devices onto old networks, leave vendor defaults in place, or assume the processor handles every security obligation. Businesses that already rely on ongoing IT operations support usually perform better because asset inventories, patch schedules, and escalation paths are maintained before a busy sales period exposes a gap.

What does balancing payment security with operational efficiency actually mean in retail?

It means reducing where card data can touch the environment while keeping checkout steps short and repeatable. Guidance in the PCI DSS Official Standards matters because retailers lose control when payment terminals, back-office PCs, printers, and remote support tools share too much trust. In mature environments, tokenization or validated point-to-point encryption, network segmentation, and tightly limited administrative access shrink the card-data environment so routine sales can move quickly without exposing unnecessary systems.

Why does this balance matter at the register and in back-office operations?

Because payment friction does not stay at the lane. A common failure point is when slow authorizations, supervisor overrides, or offline transaction fallbacks spill into refunds, inventory updates, reconciliation, and customer-service calls; the same workflow lesson appears in other industries, including IT challenges in healthcare practices, where controls often fail when they are added without regard for frontline process. In retail, weak alignment usually shows up as longer lines, more manual exceptions, higher chargeback exposure, and staff creating workarounds that introduce new security gaps.

What risks are retailers actually reducing when they tighten payment controls?

Retailers are reducing cardholder data exposure, fraudulent refunds, credential abuse in cloud POS portals, malware movement from non-payment devices, and audit problems after disputed transactions. In environments that have not been reviewed recently, shared cashier accounts, dormant vendor logins, and reused local administrator passwords are common; guidance from NIST SP 800-63B matters here because authentication only works when identity is managed through the full account lifecycle, not just at login. The control is least-privilege access with enforced multifactor authentication for administrative and remote access, supported by regular account reviews so former staff, temporary contractors, and unused support accounts do not remain inside the payment environment.

How does a secure and efficient payment environment work in practice?

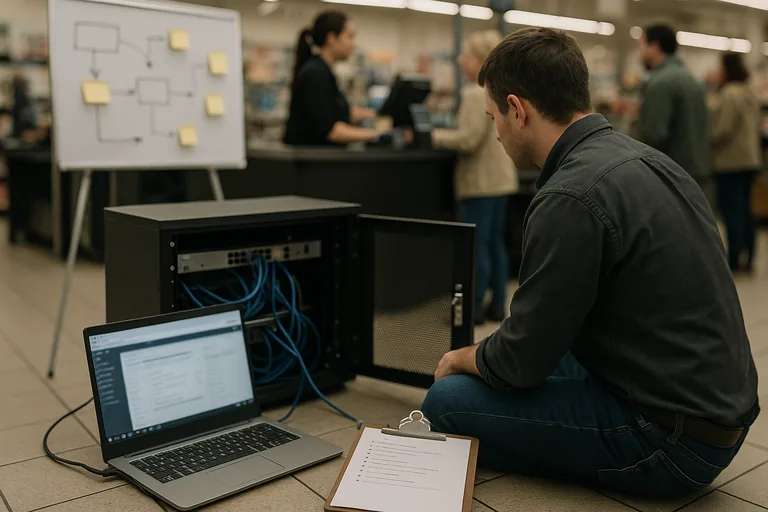

In practice, efficient security starts with separating POS terminals from guest Wi-Fi, office workstations, cameras, and general browsing, then routing payment traffic through hardened systems with documented patch windows, vendor access rules, and alerting on terminal health and transaction latency. During one routine review pattern, repeated authorization slowdowns on a single lane led investigators to find that a store switch had been reconfigured so POS traffic and guest Wi-Fi shared the same congested uplink, while a back-office PC on that flat network still had remote administrative rights to a receipt printer. The lesson was not that the hardware failed; it was that segmentation, change control, and performance monitoring have to work together if security is going to support speed instead of degrading it.

How can a business owner tell whether controls are real or just assumed?

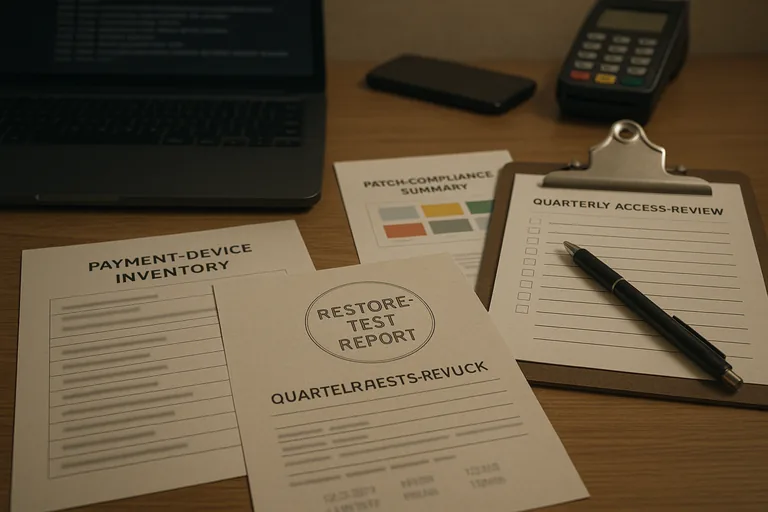

A competent provider or internal team should be able to show a current payment-device inventory, patch compliance reports for POS endpoints, quarterly access review records, firewall or segmentation diagrams, failed-login and alert-escalation logs, and documented procedures for store openings, closings, refunds, and offline card handling. This is where disciplined managed IT operations become visible as evidence rather than promises. Without those records, businesses often assume the environment is covered until an incident reveals that one terminal was missed in patching, a former employee still had refund permissions, or security alerts were going to an unattended mailbox.

When does weak implementation become dangerous?

Weak implementation becomes dangerous when controls exist on paper but not in enforced practice. A common failure point is vendor remote access left permanently enabled, endpoint protection installed but excluded from POS directories to avoid troubleshooting, or multifactor authentication required for headquarters staff but not for third-party support accounts; this tends to break down during holidays, turnover, and store expansions, when shortcuts are taken to keep lanes open. The operational consequence is predictable: fraud investigations take longer, payment outages spread farther, and the business learns too late that speed was being preserved by bypassing the very controls meant to protect revenue.

What should retail leaders do next to improve security without slowing sales?

If long lines, manual card entry, or uncertainty around payment controls sound uncomfortably close to the tension in Ashton W.’s situation, it may be time to speak with an experienced advisor before the next high-volume sales period turns a manageable gap into another $75,750 problem.